Equipment Finance vs Leasing: Which Option Suits Your Business?

May 20, 2026

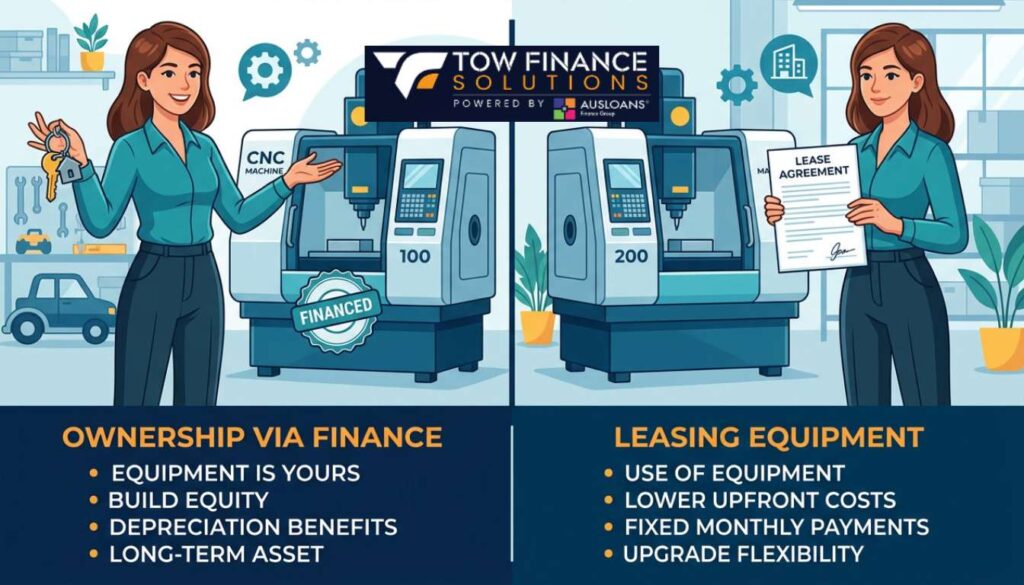

Equipment finance gives you ownership of the asset from day one, while leasing lets you use it without owning it. The best choice depends on your tax position, cash flow, and whether you plan to keep the equipment long term. For most Australian small businesses seeking immediate tax deductions and equity in their assets, equipment finance (typically structured as a chattel mortgage) is the stronger option. Leasing suits businesses that upgrade frequently or prefer predictable operating expenses.

According to the Australian Bureau of Statistics, business investment in machinery and equipment rose 13% in the September quarter of 2025, the strongest quarterly jump in over four years. Australian companies are planning to invest $202.8 billion in capital expenditure during FY26, a 7.4% increase on the prior year. With that level of spending, choosing the right funding structure is not a minor detail. It directly affects your bottom line.

Tow Finance Solutions works with over 40 lenders to match your business with the right finance structure for equipment purchases, whether that is a chattel mortgage, hire purchase, finance lease, or operating lease. This guide breaks down both options so you can move forward with confidence.

Key Takeaways

- Equipment finance (chattel mortgage) provides immediate asset ownership, GST credits, and depreciation deductions.

- Leasing (finance lease or operating lease) keeps the asset off your balance sheet and allows regular upgrades.

- The ATO’s $20,000 instant asset write-off applies until 30 June 2026 for owned assets only, not leased ones.

- Chattel mortgage rates in 2025 typically range from 7% to 11% p.a., while finance lease rates sit around 8% to 12% p.a.

- Around 65% of Australian business vehicle and equipment finance uses chattel mortgage structures.

- A finance broker like Tow Finance Solutions can compare both options across 40+ lenders in as little as one hour.

Find The Best Deal

With over 10 years of industry experience we are a leading independent broker with a diverse panel of 40 + lenders to find you the best solution, tailored to you and your goals!

What Is Equipment Finance?

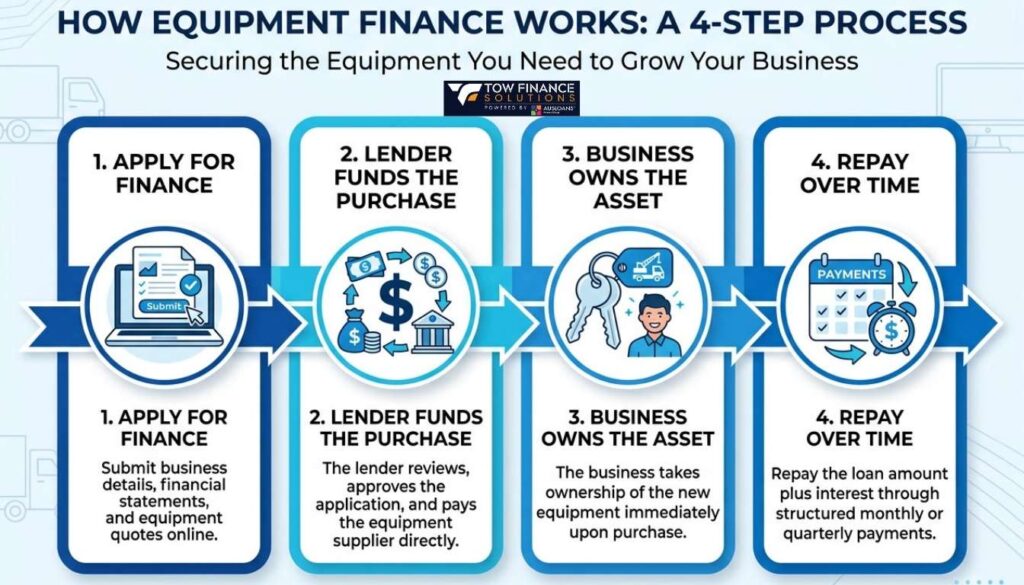

Equipment finance is a loan used to purchase business assets outright. Your business takes ownership immediately, and the lender holds the asset as security until the loan is fully repaid. The most common structure in Australia is the chattel mortgage, which literally means a “mortgage over moveable goods.”

Under a chattel mortgage, you borrow the full purchase price (minus any deposit), then repay in fixed monthly instalments over 1 to 7 years. You can include an optional balloon payment (also called a residual) at the end of the term, which lowers your monthly repayments but leaves a lump sum owing at maturity.

According to Money.com.au borrower data from 2025, the average chattel mortgage amount requested for vehicles is $71,430, and $157,728 for machinery or equipment. The vast majority of requests (84%) come from small businesses with 1 to 10 employees.

Because you own the asset from settlement, you can claim depreciation, deduct the interest component of repayments, and recover the full GST on the purchase price in your next BAS quarter. This combination of tax advantages is the primary reason chattel mortgages dominate Australian business finance.

“Chattel mortgage is often the most tax-effective option for GST-registered businesses using the cash accounting method. It allows immediate GST claims and depreciation deductions,” notes the Australian asset finance industry guidance published by Easy Asset Finance in 2025.

What Is Leasing?

Leasing allows your business to use equipment for a fixed period without purchasing it. The financier buys the asset and rents it to you under agreed terms. At the end of the lease, you typically choose between returning the equipment, extending the lease, or purchasing it at the residual value.

There are two main types of leases relevant to Australian businesses:

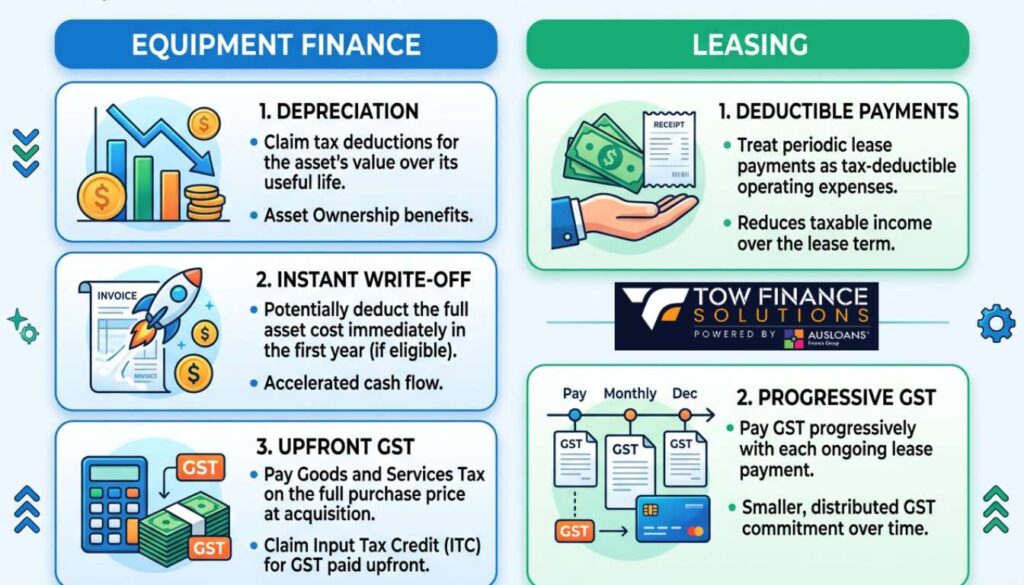

Finance Lease: The lender owns the asset, but the risks and rewards of ownership effectively transfer to you. The asset usually appears on your balance sheet under AASB 16 accounting standards. You make regular lease payments, and GST is claimed progressively on each payment rather than upfront. You cannot claim depreciation because you do not legally own the asset.

Operating Lease: The lender retains both ownership and the risks of ownership. Payments are treated as a pure operating expense, and the asset stays off your balance sheet entirely. This structure is common for equipment with rapid obsolescence, like IT hardware or medical technology.

According to industry data, finance leases account for roughly 25% of Australian business asset finance arrangements, with the remaining 10% split between hire purchase and other structures. Leasing is particularly popular among businesses that rotate equipment every 2 to 4 years or need to preserve working capital for other priorities.

If you are weighing your loan options, understanding how leasing differs from secured ownership structures is essential.

Equipment Finance vs Leasing: Side-by-Side Comparison

The table below compares the two structures across the factors that matter most to Australian business owners.

Feature | Equipment Finance (Chattel Mortgage) | Leasing (Finance Lease) |

Ownership | You own the asset from day one | Lender owns the asset during the term |

GST Treatment | Full GST claimed upfront on next BAS | GST claimed progressively on each payment |

Depreciation | Claimable under ATO schedules | Not claimable (lender owns the asset) |

Interest Deductions | Interest component is tax-deductible | Entire lease payment is tax-deductible |

Instant Asset Write-Off | Eligible (assets under $20,000, turnover under $10M) | Not eligible |

Balance Sheet | Asset and liability both recorded | May appear under AASB 16 requirements |

Typical Rates (2025) | 7% to 11% p.a. | 8% to 12% p.a. |

End of Term | You own the asset outright | Return, extend, or purchase at residual |

Best For | Long-term assets, tax maximisation | Frequent upgrades, lower monthly outlay |

This comparison highlights why the decision is not simply about monthly repayments. The tax and cash flow implications differ substantially depending on your business structure and goals.

Tax Implications: What the ATO Says

Tax treatment is the single biggest differentiator between equipment finance and leasing. Understanding how the ATO treats each structure prevents costly mistakes.

Instant Asset Write-Off (2025-26)

The Australian Government extended the $20,000 instant asset write-off until 30 June 2026 under the Treasury Laws Amendment (Strengthening Financial Systems and Other Measures) Act 2025. Small businesses with aggregated turnover under $10 million can immediately deduct the full cost of eligible assets costing less than $20,000 per item.

This benefit only applies when you own the asset. Under a chattel mortgage or hire purchase, the business takes ownership at settlement, making the asset eligible. Under a finance lease, the lender retains ownership, so the write-off does not apply. For a $19,500 asset purchased under a chattel mortgage, a business on the 25% small business tax rate saves approximately $4,875 in tax that financial year. Under a finance lease, that saving is unavailable.

Depreciation

Owned assets are depreciated according to ATO effective life schedules. You can choose either the diminishing value method (which front-loads deductions in earlier years) or the prime cost method (which spreads deductions evenly). Assets worth $20,000 or more are placed into the small business depreciation pool at 15% in the first year and 30% in subsequent years.

With a finance lease, you cannot claim depreciation because the lender owns the asset. Instead, the entire lease payment is deductible as an operating expense. For businesses with seasonal cash flow, that predictable deduction can simplify tax planning.

GST Credits

Under a chattel mortgage, a GST-registered business claims the full GST on the purchase price in the BAS quarter the asset is acquired. For a $60,000 commercial vehicle, that is a $6,000 GST credit returned to your business almost immediately.

Under a finance lease, GST is claimed incrementally on each lease payment. The total GST recovered over the lease term is the same, but you do not get the large upfront cash flow benefit.

Note: For passenger vehicles, the ATO caps the GST credit at 1/11th of the car depreciation limit. For 2025-26, the car limit is $69,674, capping the maximum GST claim at $6,334.

When Equipment Finance Is the Better Choice

Equipment finance is the stronger option when your business wants to build equity and maximise tax deductions. Choose this structure if:

- You plan to keep the equipment for 5 or more years.

- Your business has strong taxable income and benefits from front-loaded depreciation.

- You are GST-registered and want the immediate cash flow boost of an upfront GST credit.

- The asset retains value over time (e.g., heavy machinery, commercial vehicles, earthmoving equipment).

- You want the freedom to modify, customise, or sell the equipment at any time without lender restrictions.

A practical example: a landscaping business purchasing a $55,000 excavator under a chattel mortgage takes ownership at settlement, claims the $5,000 GST back on the next BAS, and begins depreciating the asset immediately. Over a 5-year term with a 20% balloon, monthly repayments are manageable, and the business builds full equity in a high-value asset.

If you are looking into vehicle financing for your fleet, chattel mortgage is the go-to structure for most Australian operators.

When Leasing Is the Better Choice

Leasing wins when flexibility and cash preservation matter more than ownership. Choose a lease if:

- You work in an industry where technology changes rapidly (IT, medical, hospitality).

- Your business upgrades equipment every 2 to 4 years.

- You want consistent, predictable monthly expenses without large upfront costs.

- You prefer not to carry the asset and associated liability on your balance sheet.

- Your cash reserves are limited and you need to preserve working capital for growth.

Operating leases, in particular, suit businesses that view equipment as a tool rather than an investment. The financier takes on the residual value risk, meaning you are not left holding an obsolete asset when the term ends.

For businesses managing cash flow fluctuations, leasing provides cost certainty that helps with budgeting.

How a Finance Broker Helps You Choose

The difference between equipment finance and leasing is not just theoretical. Rate spreads, lender policies, and tax implications vary significantly depending on the asset type, your business structure, and your credit profile.

A finance broker compares options across multiple lenders and structures, rather than locking you into a single bank’s product. According to ABS data, around 97.3% of Australian businesses are small businesses, and most lack the in-house expertise to navigate complex asset finance structures alone.

Tow Finance Solutions gives you access to 40+ lenders, with loan approvals in as little as one hour. Whether you need a chattel mortgage for a $200,000 excavator or a finance lease for $15,000 worth of IT hardware, Tow Finance Solutions’ dedicated consultants guide you through every step of the process.

Working with a broker also helps protect your credit score because your application is matched to lenders most likely to approve, reducing unnecessary hard inquiries.

Frequently Asked Questions

What is the main difference between equipment finance and leasing?

Equipment finance (chattel mortgage) gives your business ownership of the asset from day one. A lease means the financier owns the asset and you pay to use it for an agreed term. Ownership determines your tax treatment, GST credits, and what happens at the end of the agreement.

Can I claim the instant asset write-off on a leased asset?

No. The ATO’s $20,000 instant asset write-off (valid until 30 June 2026) requires that your business owns the asset. Under a finance lease, the lender retains ownership, so the deduction is not available. You would need a chattel mortgage or hire purchase structure to qualify.

Which option has lower monthly repayments?

Leasing typically offers lower monthly payments because the residual value is built into the structure. Chattel mortgages can achieve comparable repayments by including a balloon payment at the end of the term, though this creates a lump sum obligation at maturity.

Is equipment finance better for tax purposes?

For most GST-registered small businesses, yes. A chattel mortgage allows you to claim the full GST upfront, deduct interest on repayments, and claim depreciation annually. Leasing offers simpler tax administration with fully deductible lease payments, but you miss out on depreciation and the instant asset write-off.

What happens at the end of a lease?

At the end of a finance lease, you can return the equipment, extend the lease, or purchase the asset at the pre-agreed residual value. With an operating lease, you typically return the equipment unless renewal is negotiated.

How do interest rates compare between equipment finance and leasing?

In 2025, chattel mortgage rates typically ranged from 7% to 11% p.a., while finance lease rates sat between 8% to 12% p.a. The rate differential of 0.5% to 1.5% reflects the lender’s residual value risk under a lease structure. A broker like Tow Finance Solutions can help secure competitive rates across both options.

Do I need a deposit for equipment finance?

It depends on the lender, asset type, and your business profile. Some lenders offer zero-deposit chattel mortgages for established businesses with strong credit. Others may require 10% to 20% upfront. Tow Finance Solutions compares loan options across its panel to find the best terms for your situation.

Can I finance second-hand equipment?

Yes. Both chattel mortgages and finance leases can be used for second-hand equipment, though lenders may impose age limits and condition requirements. The ATO’s instant asset write-off does not distinguish between new and used assets, provided all other eligibility criteria are met.

What types of equipment can I finance or lease?

Virtually any business asset qualifies, including vehicles, trucks, excavators, medical equipment, hospitality fit-outs, IT hardware, manufacturing machinery, and agricultural equipment. Tow Finance Solutions arranges finance across a wide range of asset categories.

How long does approval take?

With Tow Finance Solutions, approvals can be completed in as little as 12-24 hours. The application process is fully online, and a dedicated consultant handles the lender comparison and paperwork on your behalf.

Take the Next Step

Choosing between equipment finance and leasing is one of the most impactful financial decisions your business will make this year. The right structure saves thousands in tax, protects your cash flow, and sets you up for long-term growth.

Tow Finance Solutions makes the process fast and simple. With access to 40+ lenders, approvals in as little as an hour, and personalised guidance from dedicated consultants, you get the right equipment finance structure for your business without the guesswork.

Apply now or call (07) 4410 3375 to speak with a Tow Finance Solutions consultant today.

Take the Next Step

Self-employed Australians deserve the same access to competitive finance as everyone else. The difference between approval and rejection often comes down to preparation, documentation, and choosing the right lender, not your employment status.

Tow Finance Solutions specialises in finding the right fit from a panel of 40+ lenders, with approvals in as little as one hour and a process built to protect your credit score. Whether you need a car, a business vehicle, or asset finance to grow your operations, the team is ready to help.

Apply online today or call (07) 4410 3375 to speak with a dedicated consultant about your self-employed finance options.

Sources

- Australian Bureau of Statistics, Private New Capital Expenditure and Expected Expenditure, Australia (December 2025): https://www.abs.gov.au/statistics/economy/business-indicators/private-new-capital-expenditure-and-expected-expenditure-australia/latest-release

- Australian Taxation Office, $20,000 Instant Asset Write-Off for 2025-26: https://www.ato.gov.au/businesses-and-organisations/small-business-newsroom/20000-instant-asset-write-off-for-2025-26

- Australian Taxation Office, Simpler Depreciation for Small Business: https://www.ato.gov.au/businesses-and-organisations/income-deductions-and-concessions/depreciation-and-capital-expenses-and-allowances/simpler-depreciation-for-small-business

- Commonwealth Bank of Australia, Business Spending September Quarter 2025: https://www.commbank.com.au/articles/newsroom/2025/11/business-spending-september-quarter.html

- Money.com.au, Australian Business Statistics 2026: https://www.money.com.au/business-loans/australian-business-statistics