Understanding Loan Pre-Qualification vs. Pre-Approval

Your Complete Guide to Getting Started Right

Nov 18, 2025

Navigating the world of financing can feel overwhelming, especially when you encounter terms like “pre-qualification” and “pre-approval.” While these terms sound similar, they represent distinctly different stages in the loan application process, each offering unique benefits and requiring different levels of commitment from both you and your lender.

Understanding the difference between pre-qualification and pre-approval is crucial for making informed financing decisions, whether you’re seeking vehicle finance, business funding, or leisure equipment loans. At Tow Finance Solutions, we help customers navigate these early stages with clarity and confidence, ensuring you choose the right path for your specific needs. Our streamlined processes and diverse network of 40+ lenders mean you can move efficiently from initial inquiry to final approval, often within hours rather than days.

Overview

This comprehensive guide will walk you through everything you need to know about loan pre-qualification and pre-approval. You’ll discover the key differences between these two processes, understand when to use each approach, and learn how to leverage both to strengthen your financing position. We’ll also explore how these preliminary steps can accelerate your final loan approval and help you secure better terms.

By the end of this article, you’ll have a clear understanding of how to approach the early stages of financing strategically, setting yourself up for success whether you’re purchasing a vehicle, expanding your business, or financing recreational equipment.

Find The Best Deal

With over 10 years of industry experience we are a leading independent broker with a diverse panel of 40 + lenders to find you the best solution, tailored to you and your goals!

Key Takeaways

- Pre-qualification provides a quick estimate based on basic information you provide, with no credit check required

- Pre-approval involves a thorough review of your financial situation, including a credit check, resulting in a conditional loan commitment

- Pre-approval carries more weight with sellers and gives you stronger negotiating power

- Both processes can help you understand your budget and financing options before making major purchases

- Pre-qualification is ideal for initial budgeting, while pre-approval is essential for serious shopping

- Neither guarantees final loan approval, but pre-approval gets you much closer to a firm commitment

- Working with experienced brokers like Tow Finance Solutions can streamline both processes significantly

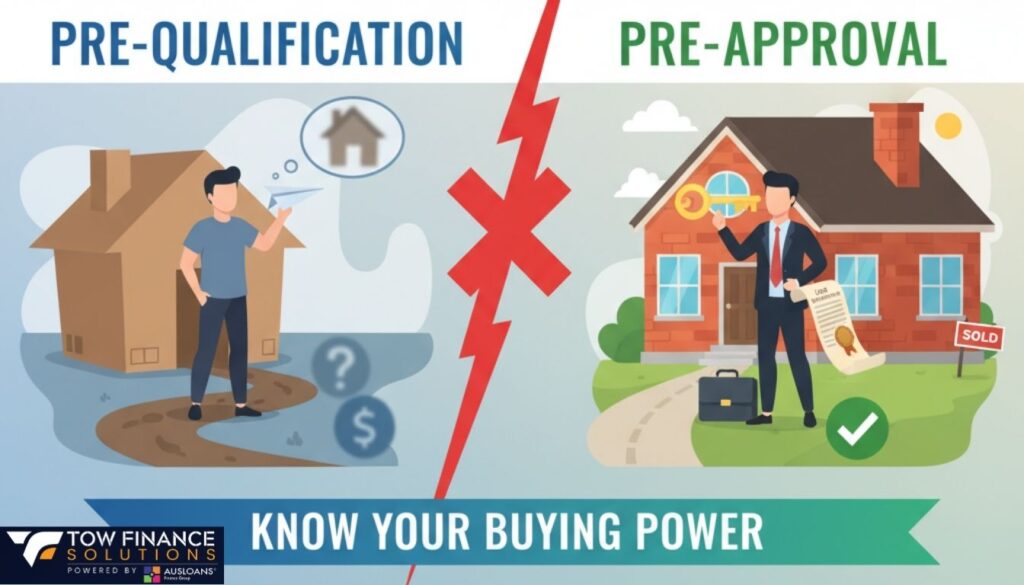

What is Loan Pre-Qualification?

The Basics of Pre-Qualification

Loan pre-qualification is an informal assessment that gives you a preliminary idea of how much you might be able to borrow and at what interest rate. This process typically involves providing basic financial information to a lender or broker, who then uses this information to estimate your borrowing capacity without conducting a formal credit check.

During pre-qualification, you’ll typically share details about your income, employment status, existing debts, and the amount you’re looking to borrow. The lender uses this information to provide an estimate based on their general lending criteria. This process is usually quick, often completed within minutes, and can frequently be done online or over the phone.

Pre-qualification serves as an excellent starting point for understanding your financing options. It helps you establish a realistic budget before you begin shopping for vehicles, equipment, or making business investments. However, it’s important to understand that pre-qualification is not a guarantee of lending, and the final terms may differ significantly once a thorough review is conducted.

Benefits of Pre-Qualification

Pre-qualification offers several advantages, particularly for those in the early stages of considering a purchase. First, it provides valuable insight into your potential borrowing capacity without any commitment from either party. This information helps you set realistic expectations and focus your search on options within your likely price range.

The process is also completely free and doesn’t impact your credit score, since most lenders perform only a soft credit inquiry or rely entirely on the information you provide. This means you can explore multiple options without concern about affecting your credit rating. Additionally, pre-qualification can often be completed quickly, sometimes within minutes, making it an efficient first step in your financing journey.

Pre-qualification also helps you understand the general market conditions and what different lenders might offer. When working with a broker like Tow Finance Solutions, pre-qualification allows you to quickly assess options across our extensive network of over 40 lenders, giving you a broad view of potential terms and conditions before committing to a formal application.

Limitations of Pre-Qualification

While pre-qualification is useful, it has significant limitations that borrowers should understand. The estimates provided are based on limited information and general lending guidelines, not a thorough review of your complete financial picture. This means the actual terms offered during formal application may vary considerably from the pre-qualification estimate.

Pre-qualification typically doesn’t include verification of the information you provide. Lenders assume the accuracy of your stated income, debts, and other financial details. When these details are formally verified during the application process, discrepancies may lead to different terms or even denial of the loan.

The preliminary nature of pre-qualification also means it carries little weight in competitive buying situations. Sellers, particularly in hot markets, may give preference to buyers with more substantial proof of financing capability. Pre-qualification alone may not be sufficient to demonstrate serious intent or financial capacity to complete a purchase.

What is Loan Pre-Approval?

Understanding the Pre-Approval Process

Loan pre-approval is a much more comprehensive evaluation that involves a thorough review of your financial situation. During this process, lenders examine your credit history, verify your income and employment, review bank statements, and assess your overall debt-to-income ratio. This detailed analysis allows them to make a conditional commitment to lend you a specific amount at predetermined terms.

The pre-approval process typically requires you to complete a formal loan application and provide extensive documentation. This might include recent pay stubs, tax returns, bank statements, and details about existing debts and assets. The lender will also perform a hard credit inquiry, which may temporarily impact your credit score but provides them with a complete picture of your credit history.

Upon successful completion of the pre-approval process, you’ll receive a pre-approval letter or certificate that specifies the loan amount, interest rate, and basic terms for which you qualify. This document represents a conditional commitment from the lender, subject to final verification and approval of the specific item you’re financing.

Advantages of Pre-Approval

Pre-approval offers significant advantages over pre-qualification, particularly when you’re ready to make serious purchase decisions. The most important benefit is the credibility it provides with sellers. A pre-approval letter demonstrates that you have undergone thorough financial scrutiny and that a lender has made a conditional commitment to finance your purchase.

This credibility can be crucial in competitive markets or when negotiating with sellers. Many sellers prefer to work with pre-approved buyers because it reduces the risk of financing-related delays or deal failures. In some cases, pre-approval can give you an advantage over other potential buyers who lack this documentation.

Pre-approval also provides you with a clear understanding of your financing terms before you begin shopping. You’ll know exactly how much you can borrow, what your interest rate will be, and what your monthly payments are likely to be. This knowledge allows you to shop with confidence and make decisions quickly when you find the right opportunity.

Pre-Approval Requirements and Timeline

The pre-approval process requires more time and documentation than pre-qualification, but the investment often pays dividends in terms of credibility and certainty. Most lenders require recent pay stubs (typically the last two months), tax returns from the previous year or two, bank statements showing account balances and transaction history, and a complete list of existing debts and monthly obligations.

Employment verification is also standard, and some lenders may contact your employer directly to confirm your position and income. Self-employed individuals may need to provide additional documentation, such as profit and loss statements or business bank statements. The specific requirements can vary between lenders and loan types.

The timeline for pre-approval varies depending on the lender and the complexity of your financial situation. With traditional lenders, the process might take several days to a week. However, experienced brokers like Tow Finance Solutions can often expedite this process significantly, sometimes achieving pre-approval within hours by leveraging relationships with lenders and streamlined application processes.

Key Differences Between Pre-Qualification and Pre-Approval

Documentation Requirements

The documentation requirements represent one of the most significant differences between pre-qualification and pre-approval. Pre-qualification typically requires only basic information that you can provide verbally or through a simple online form. This might include your estimated income, employment status, approximate debt levels, and the loan amount you’re considering.

Pre-approval, in contrast, requires extensive documentation to verify every aspect of your financial situation. Lenders want to see proof of income through pay stubs and tax returns, verification of assets through bank statements, confirmation of employment, and detailed information about existing debts and obligations. This documentation allows lenders to make informed decisions based on verified facts rather than estimates.

The documentation phase of pre-approval can be time-consuming, but it’s also where much of the value lies. By thoroughly reviewing your financial situation upfront, lenders can provide more accurate terms and identify potential issues before you find something you want to purchase. This thorough review also means that final approval is typically much faster once you’ve identified your specific purchase.

Credit Impact Considerations

One of the most important practical differences between pre-qualification and pre-approval relates to the impact on your credit score. Pre-qualification typically involves only a soft credit inquiry, which doesn’t affect your credit score. Some pre-qualification processes don’t involve any credit check at all, relying entirely on the information you provide.

Pre-approval almost always requires a hard credit inquiry, which can temporarily lower your credit score by a few points. However, this impact is generally minimal and short-lived, especially if you’re not applying for multiple types of credit simultaneously. The credit bureaus recognize that consumers often shop around for the best rates, so multiple inquiries for the same type of loan within a short period are typically treated as a single inquiry.

When working with brokers like Tow Finance Solutions, it’s important to understand that we use processes designed to minimize negative impact on your credit score. Our experienced team can often determine the best lender options before initiating formal applications, reducing the number of hard inquiries needed to secure optimal financing.

Level of Commitment

The level of commitment from both parties differs significantly between pre-qualification and pre-approval. Pre-qualification represents minimal commitment from either side. The lender provides estimates based on limited information, and you’re under no obligation to proceed with that lender or even to pursue financing at all.

Pre-approval represents a much higher level of commitment from the lender. After thoroughly reviewing your financial situation, the lender makes a conditional commitment to provide financing at specific terms. While this commitment is still subject to final approval and verification of the item being financed, it represents a much stronger assurance than pre-qualification.

From your perspective, pursuing pre-approval also represents a higher level of commitment to moving forward with a purchase. The time and effort required to gather documentation and complete the application process indicates serious intent to proceed with financing. This mutual commitment often leads to smoother transactions and faster final approvals.

When to Choose Pre-Qualification vs. Pre-Approval

Ideal Scenarios for Pre-Qualification

Pre-qualification is ideal when you’re in the early stages of considering a purchase and want to understand your general financing options without making a firm commitment. If you’re still deciding whether to buy a vehicle, expand your business, or make another significant purchase, pre-qualification can help you understand what might be possible without affecting your credit score.

Pre-qualification is also useful when you want to compare options across multiple lenders or types of financing. Since the process is quick and doesn’t impact your credit, you can easily gather estimates from various sources to understand the range of terms available. This information can help you make informed decisions about timing, loan amounts, and which lenders to pursue for formal applications.

If you’re planning a purchase several months in the future, pre-qualification can help you understand what steps you might need to take to improve your financing position. For example, you might discover that paying down certain debts or increasing your down payment could significantly improve your terms. This early insight allows you to take action before you need financing.

When Pre-Approval Makes Sense

Pre-approval is essential when you’re ready to make serious purchase decisions and want the credibility and negotiating power that comes with verified financing. If you’re planning to shop for vehicles, equipment, or other financed items within the next few weeks or months, pre-approval ensures you can act quickly when you find the right opportunity.

Pre-approval is also valuable when you’re entering competitive markets where sellers have multiple options. Having pre-approval documentation demonstrates that you’re a serious buyer with verified financing capability. This can be particularly important for business equipment purchases or in markets where financing contingencies might make your offer less attractive.

If you have a complex financial situation, pre-approval can help identify and resolve potential issues before you find something you want to purchase. Self-employed individuals, those with recent credit issues, or buyers with non-traditional income sources often benefit from addressing any documentation or qualification concerns early in the process.

Strategic Timing Considerations

The timing of when you pursue pre-qualification versus pre-approval can significantly impact your financing experience. Generally, it’s wise to start with pre-qualification early in your consideration process, then move to pre-approval as you get closer to making a purchase decision.

For most purchases, pursuing pre-approval 30-60 days before you plan to buy provides optimal timing. This gives you enough time to address any issues that arise during the approval process while ensuring the pre-approval remains current when you’re ready to purchase. Most pre-approval letters are valid for 60-90 days, though specific timeframes vary by lender.

It’s also important to consider market conditions when timing your pre-approval. In fast-moving markets, having current pre-approval can be crucial for making competitive offers. However, if you’re planning to shop for an extended period, you might want to delay pre-approval until closer to your purchase timeline to ensure the terms remain current and valid.

Impact on Your Credit Score

Understanding Credit Inquiries

When considering pre-qualification and pre-approval, it’s essential to understand how each process affects your credit score. Credit inquiries fall into two categories: soft inquiries and hard inquiries. Soft inquiries don’t affect your credit score and include things like checking your own credit, pre-qualification assessments, and background checks by existing creditors.

Hard inquiries do impact your credit score and occur when you formally apply for credit. These inquiries can lower your score by a few points, typically 2-5 points, and remain on your credit report for two years. However, their impact on your score diminishes over time, with most of the effect disappearing after about six months.

The good news is that credit scoring models recognize that consumers often shop around for the best rates on loans. When you have multiple hard inquiries for the same type of loan within a short period (typically 14-45 days, depending on the scoring model), they’re usually treated as a single inquiry for scoring purposes. This allows you to compare offers without dramatically impacting your credit score.

Managing Multiple Applications

If you’re considering multiple financing options, it’s important to manage the timing of your applications strategically. For pre-qualification, since most processes use soft inquiries, you can generally explore multiple options without credit score concerns. This allows you to gather a comprehensive view of your options before moving to formal applications.

For pre-approval, it’s wise to complete your shopping within a focused timeframe to take advantage of the inquiry grouping mentioned above. At Tow Finance Solutions, we help manage this process by identifying the best lender options based on your profile before initiating formal applications. This targeted approach minimizes the number of hard inquiries needed.

It’s also important to avoid applying for other types of credit during your financing process. If you’re shopping for vehicle finance, avoid applying for credit cards, personal loans, or other unrelated credit products during the same period. Multiple types of credit inquiries don’t benefit from the same grouping treatment and can have a more significant impact on your score.

Protecting Your Credit During the Process

There are several steps you can take to protect your credit score during the financing process. First, be honest and accurate about your intentions when speaking with lenders. If you’re just exploring options, make it clear that you’re seeking pre-qualification rather than formal pre-approval. This helps ensure that only soft inquiries are performed.

When you’re ready for pre-approval, gather all necessary documentation before beginning the process. Having everything ready allows you to complete applications quickly and efficiently, reducing the timeframe over which hard inquiries occur. This organization also demonstrates preparation to lenders, which can positively influence their decision-making process.

Consider working with experienced brokers like Tow Finance Solutions who understand credit protection strategies. Our team can help you navigate the process in a way that minimizes credit impact while maximizing your approval chances. We understand which lenders are most likely to approve your application, reducing the need for multiple attempts.

Common Misconceptions and Mistakes

Myths About Pre-Qualification and Pre-Approval

One common misconception is that pre-qualification and pre-approval are guarantees of final loan approval. While both processes provide valuable insights into your likely approval and terms, neither represents a firm commitment to lend. Pre-qualification is particularly preliminary, based on limited information and general guidelines rather than thorough verification.

Another myth is that pre-approval locks in your interest rate permanently. Most pre-approval letters include rate estimates based on current market conditions, but final rates are typically determined at the time of loan closing. Interest rates can change between pre-approval and final approval, particularly if market conditions shift or if there’s a significant delay between approval and purchase.

Some borrowers also believe that once they’re pre-approved with one lender, they can’t or shouldn’t explore other options. In reality, pre-approval from one lender can actually strengthen your position when negotiating with others. Having a firm offer in hand gives you leverage and confidence when exploring alternative financing options.

Documentation Errors to Avoid

One of the most common mistakes in the pre-approval process is providing incomplete or inaccurate documentation. This might include outdated pay stubs, incomplete tax returns, or bank statements that don’t show required time periods. These errors can delay the approval process significantly and may require starting over with updated documentation.

Another frequent error is failing to disclose existing debts or obligations. Some applicants focus only on major debts like mortgages and car loans while overlooking credit card balances, personal loans, or other obligations. Lenders will discover these debts during their review, and failing to disclose them upfront can damage your credibility and potentially lead to denial.

Self-employed borrowers often struggle with documentation requirements, sometimes providing business documents when personal income verification is needed, or vice versa. Understanding exactly what documentation is required for your employment situation is crucial for a smooth approval process. Working with experienced professionals can help ensure you provide the right documents in the right format.

Timing and Expectation Mistakes

Many borrowers make timing mistakes that can complicate their financing process. Starting the pre-approval process too early might result in expired approvals by the time you’re ready to purchase. Starting too late might leave you scrambling to complete documentation while trying to finalize a purchase, potentially missing opportunities or accepting less favorable terms.

Unrealistic expectations about approval timelines can also cause problems. While some lenders can provide quick decisions, complex applications or unusual circumstances may require additional time for review. Planning for potential delays and starting the process with adequate buffer time helps ensure you’re not pressured into poor decisions.

Another common mistake is assuming that the first pre-approval offer is the best available. Different lenders have different strengths and preferences, and terms can vary significantly between institutions. Taking time to compare offers, especially when working with brokers who have access to multiple lenders, often results in better terms and conditions.

Tips for a Successful Application Process

Preparing Your Financial Documentation

Success in both pre-qualification and pre-approval often comes down to preparation and organization. Start by gathering all potentially required documents before beginning any formal application process. This includes recent pay stubs, tax returns, bank statements, documentation of other income sources, and a list of all existing debts and monthly obligations.

For employed individuals, ensure your pay stubs are recent (typically within 30 days) and clearly show year-to-date earnings. If you’ve recently changed jobs, be prepared to provide documentation from both your current and previous employers. Employment gaps or changes may require additional explanation, so prepare clear, honest explanations for any unusual circumstances.

Self-employed individuals should focus on demonstrating stable, consistent income through tax returns, profit and loss statements, and business bank statements. Having an accountant prepare or review your financial documentation can add credibility and ensure everything is presented clearly and professionally.

Optimizing Your Application Timing

Timing your application strategically can significantly impact your success and the terms you receive. Generally, avoid applying during periods when your financial situation is in flux, such as immediately after changing jobs, during tax season when processing might be slower, or when you’re carrying unusually high credit card balances.

Consider the timing of large purchases or financial changes that might affect your application. For example, if you’re planning to pay off credit cards or make a large deposit, consider completing these actions before applying if they’ll improve your financial profile. However, avoid making major financial changes during the application process without discussing them with your lender first.

Market conditions can also affect timing. Interest rates, lender appetite for certain types of loans, and seasonal factors can all influence the terms available to you. Experienced brokers like Tow Finance Solutions can provide guidance on market timing and help you understand when conditions might be most favorable for your application.

Working Effectively with Lenders and Brokers

Communication is key to a successful financing experience. Be honest and upfront about your financial situation, including any challenges or unusual circumstances. Lenders and brokers are experienced in working with various situations, and early disclosure of potential issues allows them to address concerns proactively rather than discovering problems later in the process.

Ask questions about anything you don’t understand, including terms, requirements, and timelines. A good lender or broker should be willing to explain the process clearly and help you understand your options. Don’t hesitate to seek clarification on documentation requirements, approval conditions, or any other aspects of the process.

When working with brokers like Tow Finance Solutions, take advantage of their expertise and lender relationships. We can provide insights into which lenders are most likely to approve your application, what terms you might expect, and how to present your application most effectively. Our experience often allows us to anticipate and address potential issues before they become problems.

Industry Best Practices and Standards

Regulatory Compliance and Consumer Protection

The lending industry operates under extensive regulatory oversight designed to protect consumers and ensure fair lending practices. The Truth in Lending Act requires lenders to provide clear disclosure of loan terms, including interest rates, fees, and payment schedules. The Equal Credit Opportunity Act prohibits discrimination based on race, gender, marital status, religion, or other protected characteristics.

These regulations extend to both pre-qualification and pre-approval processes. Lenders must provide accurate information about potential terms and cannot mislead consumers about their likelihood of approval or the terms they might receive. When rate ranges are provided, they must be based on actual lending decisions rather than theoretical minimums that few borrowers could achieve.

At Tow Finance Solutions, we ensure all our processes comply with applicable regulations and industry standards. Our team stays current with regulatory changes and works only with lenders who maintain high standards of compliance and customer service. This commitment to regulatory compliance protects both our customers and our business relationships.

Professional Standards in Finance Brokerage

Professional finance brokers adhere to industry standards that prioritize customer service, transparency, and ethical conduct. This includes providing clear explanations of the brokerage process, disclosing all fees and compensation arrangements, and maintaining confidentiality of customer financial information.

Quality brokers also maintain ongoing relationships with diverse lender networks and stay current with changing lending criteria and market conditions. This knowledge allows them to provide accurate guidance and match customers with appropriate lending options based on current market realities rather than outdated information.

Continuing education and professional development are also hallmarks of reputable finance brokers. The lending industry evolves constantly, with new products, regulations, and market conditions requiring ongoing learning and adaptation. At Tow Finance Solutions, our team participates in regular training and maintains industry certifications to ensure we provide the most current and accurate guidance to our customers.

Technology and Security Standards

Modern lending processes rely heavily on technology for application processing, document management, and communication. Industry-standard security measures include encryption of sensitive data, secure document transmission, and multi-factor authentication for access to customer information.

Reputable lenders and brokers also maintain appropriate insurance coverage and bonding to protect customer interests. This includes professional liability insurance, errors and omissions coverage, and in some cases, bonding requirements that provide additional protection for customer funds and information.

At Tow Finance Solutions, we use industry-leading technology platforms that meet or exceed security standards for financial services. Our systems are regularly audited and updated to ensure customer information remains secure throughout the application and approval process. We also maintain transparent policies about data use and sharing, giving customers clear understanding of how their information is handled.

Frequently Asked Questions

What’s the main difference between pre-qualification and pre-approval? Pre-qualification is a quick estimate based on basic information you provide, while pre-approval involves thorough verification of your finances including a credit check. Pre-approval results in a conditional loan commitment, whereas pre-qualification is just an estimate.

Does pre-qualification affect my credit score? No, pre-qualification typically uses only a soft credit inquiry or no credit check at all, so it won’t impact your credit score. You can explore multiple pre-qualification options without any credit concerns.

How long does pre-approval take? Pre-approval timelines vary by lender and application complexity. At Tow Finance Solutions, we often achieve pre-approval in as little as one hour for well-prepared applications, though complex situations may take longer.

Can I shop around after getting pre-approved? Yes, you can continue shopping for better terms even after pre-approval. Having a pre-approval in hand actually strengthens your negotiating position with other lenders and shows sellers you’re a serious buyer.

How long is pre-approval valid? Most pre-approval letters are valid for 60-90 days, though specific timeframes vary by lender. Some lenders may extend or update pre-approvals if your financial situation remains stable.

What documents do I need for pre-approval? Typical requirements include recent pay stubs, tax returns, bank statements, employment verification, and a list of existing debts. Self-employed individuals may need additional business documentation.

Will pre-approval guarantee my loan? Pre-approval is a conditional commitment based on verification of your finances, but final approval depends on the specific item being financed and final underwriting review. It’s much stronger than pre-qualification but not a final guarantee.

Can I get pre-approved for different loan amounts? Yes, you can pursue pre-approval for different amounts or from multiple lenders. Just be mindful that each formal application may result in a hard credit inquiry, so plan your applications strategically.

Should I get pre-qualified or pre-approved first? Start with pre-qualification to understand your general options, then move to pre-approval when you’re ready to shop seriously. Pre-qualification helps with initial budgeting, while pre-approval gives you credibility with sellers.

How does working with a broker affect these processes? Brokers like Tow Finance Solutions can streamline both processes by matching you with suitable lenders from their network, reducing the number of applications needed and often achieving better terms through established relationships.

Sources

- Australian Securities and Investments Commission (ASIC) – Consumer Credit Information: https://www.asic.gov.au

- Reserve Bank of Australia – Interest Rates and Monetary Policy: https://www.rba.gov.au

- Australian Prudential Regulation Authority (APRA) – Banking Standards: https://www.apra.gov.au

- Fair Trading NSW – Consumer Credit Protection: https://www.fairtrading.nsw.gov.au

- Australian Competition and Consumer Commission (ACCC) – Consumer Rights: https://www.accc.gov.au

- Credit Ombudsman Service Australia – Consumer Protection: https://www.cosl.com.au

Ready to move forward with confidence? Whether you’re interested in pre-qualification to explore your options or ready for pre-approval to strengthen your purchasing power, contact our expert team today. With access to over 40 lenders and approvals possible in as little as one hour, Tow Finance Solutions makes your financing journey simple, fast, and successful.