Hybrid Caravan and Camper Trailer Finance: A Complete Buyer's Guide

June 25, 2026

Yes, you can finance a hybrid caravan or camper trailer in Australia, usually through a secured leisure loan over one to seven years, with no deposit required and approvals often turned around in as little as one hour. A hybrid caravan finance arrangement uses the van itself as security, which keeps interest rates lower than an unsecured personal loan. This guide explains how the finance works, what it costs in 2026, and how to get approved fast.

Hybrid caravans sit between a rugged camper trailer and a full touring caravan, and that middle ground is exactly why they have surged in popularity. Caravan and campervan registrations reached almost 938,000 in 2025, a 32% increase since 2019 and an all-time record, according to Tourism Research Australia. Financing one well comes down to choosing the right loan structure, not just the lowest advertised rate.

Overview

This guide covers what a hybrid caravan actually is, how much you should expect to pay, current finance rates and loan terms, the secured-versus-unsecured decision, what lenders assess, and how to speed up approval. It finishes with a detailed FAQ and the documents you need to apply.

Key Takeaways

- Hybrid caravans combine camper trailer toughness with caravan comfort, typically priced between $39,000 and $97,000 new.

- Secured loans use the van as collateral and carry lower rates than unsecured personal loans.

- Loan terms run from one to seven years, with no deposit needed in most cases.

- New-model loans averaged around 8.65% p.a. in 2025; used models averaged higher.

- The average Australian caravan loan is $48,406, sitting squarely in the hybrid price bracket.

- Pre-approval lasts 30 to 90 days and lets you shop with a firm budget.

Find The Best Deal

With over 10 years of industry experience we are a leading independent broker with a diverse panel of 40 + lenders to find you the best solution, tailored to you and your goals!

What Is a Hybrid Caravan or Camper Trailer?

A hybrid caravan is a compact, off-road-capable van that blends the lightweight, go-anywhere build of a camper trailer with the hard walls, fixed bed and internal amenities of a full caravan. Unlike a soft-floor camper, a hybrid has a solid roof and body, so it protects you from harsh weather while still being light enough to tow off the bitumen.

The category matters for finance because weight and use change how a lender views the asset. A hybrid is classified as a towable recreational vehicle, the same category that captured 63.37% of the Australian recreational vehicle market in 2025.

Hybrids usually feature independent off-road suspension, a DO35-style hitch coupling (a heavy-duty articulating tow connection built for rough terrain), lithium batteries and solar for off-grid power. These inclusions add value but also add to the price, which is why understanding finance structure early pays off.

Most buyers fall into one of three groups: couples chasing remote tracks, young families wanting a flexible weekender, and grey nomads who want comfort without towing a large van. Private buyers accounted for 78.17% of the recreational vehicle market in 2025.

How Much Does a Typical Hybrid Caravan Cost in Australia?

Expect to pay between $39,000 and $97,000 for a new hybrid caravan, with most family-ready models landing in the $45,000 to $65,000 range. Budget hybrids from established brands start around $43,000, while premium tandem-axle, fully off-grid units climb toward $90,000 and beyond.

For context, the most affordable new hybrids in 2025 included models priced from the low-to-mid $40,000s, typically offering a queen bed, lithium power and an external kitchen. Used hybrids can be found from the high $30,000s, which lowers your borrowing amount but may attract a higher interest rate.

These price points sit right at the national average. The average caravan loan amount in Australia is $48,406, while campervan borrowers average $37,975, according to Money.com.au borrower data. If you are weighing whether now is the right time to buy, our guide on borrowing during inflation is worth a read.

Hybrid Type | Typical Price (New) | Common Loan Amount | Best-Suited Loan Term |

Compact couples hybrid | $40,000–$50,000 | $40,000–$48,000 | 3–5 years |

Family pop-top hybrid | $48,000–$65,000 | $45,000–$60,000 | 5–7 years |

Premium off-grid hybrid | $65,000–$97,000 | $60,000–$90,000 | 5–7 years |

Hybrid Caravan Finance: Rates and Loan Terms in 2026

Secured hybrid caravan loans generally carry fixed interest rates, with terms from one to seven years and no deposit required. A fixed rate means your repayment stays the same for the full loan, making it easy to budget regardless of what the Reserve Bank does next.

Rates vary by lender, the age of the van, and your credit profile. The average interest rate for new caravan loans in 2025 was 8.65% p.a., while the average for used models rose to 11.93% p.a., according to Savvy. Across the market, caravan loan interest rates generally range from about 5.35% p.a. to 14.99% p.a., with the strongest applicants securing the lowest end.SavvyFinder

Interest rates have firmed up recently. The RBA held the cash rate at 4.35% in June 2026 after three increases earlier in the year, which has kept fixed leisure-loan rates elevated. Locking in a fixed rate now removes the uncertainty of further movement.A balloon payment can lower your monthly repayments by deferring a lump sum to the end of the term, though you pay more interest overall. If that structure interests you, see how balloon payments work before you commit, and use a loan calculator to compare scenarios.

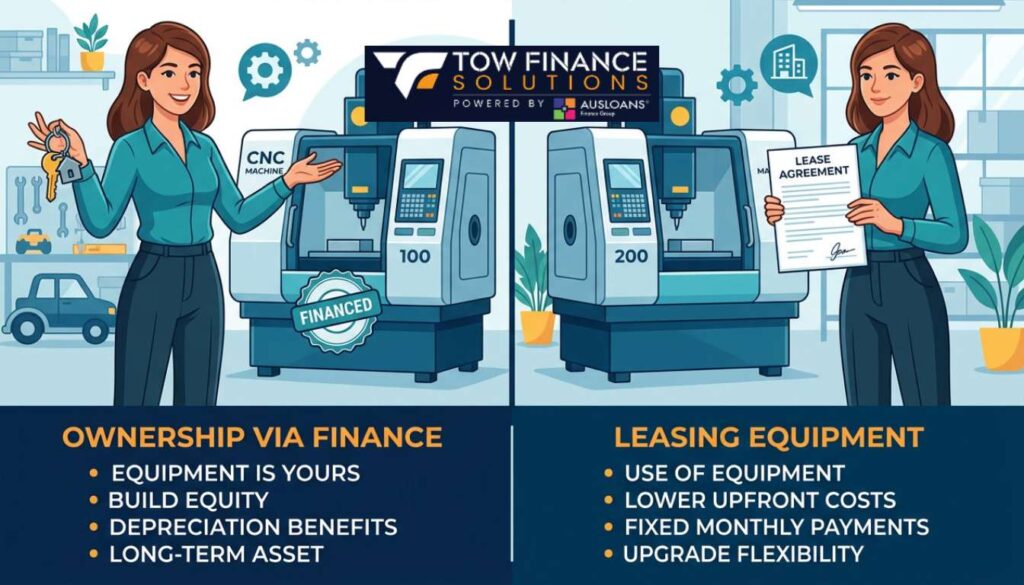

Secured vs Unsecured: Which Loan Should You Choose?

The best choice for most buyers is a secured loan, because using the hybrid as collateral lowers the lender’s risk and your rate. Lenders typically advance up to 100% of the van’s value on a secured loan, so you can drive away without a deposit.

An unsecured loan offers more flexibility, since the funds are not tied to the asset and can cover extras the lender may not include under secured finance. The trade-off is cost. Unsecured rates run higher because the lender has no asset to recover if repayments stop.

Feature | Secured Loan | Unsecured Loan |

Interest rate | Lower (van is collateral) | Higher |

Deposit | Often none required | Often none required |

Borrowing limit | Up to 100%+ of value | Generally lower |

Covers accessories | Limited | More flexible |

Risk if you default | Van can be repossessed | No asset taken directly |

For a deeper breakdown, read our secured vs unsecured comparison. According to ASIC, lenders holding a credit licence must ensure any loan is not unsuitable for the consumer, so a reputable broker will match the structure to your situation rather than push the highest-margin product.

What Lenders Assess Before Approving Your Loan

Lenders approve hybrid caravan finance based on your income stability, existing debts, credit history, and the age and value of the van. A homeowner in full-time employment will generally receive a sharper rate than a casual worker who rents, because the application carries less perceived risk.

The van itself is also assessed. Some lenders will only finance caravans up to a certain age, for example under 10 years old at the end of the loan term, which protects their security in case of default. Older or rarer models can attract a rate loading.

Your credit score is one of the biggest levers you control. If yours needs work, our credit score guide walks through five practical steps, and the common mistakes article helps you avoid the errors that slow approvals down.

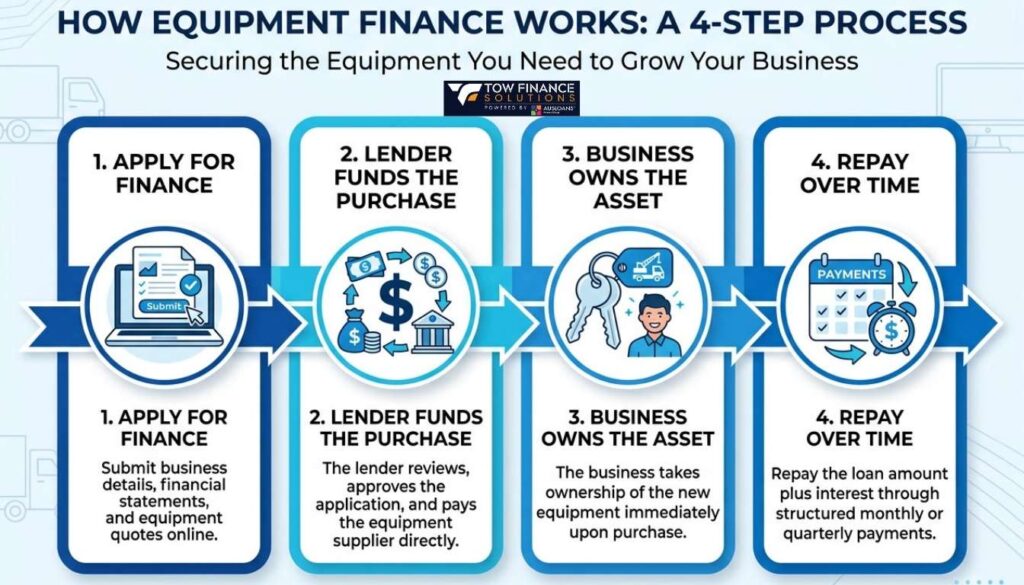

How to Get Approved Fast

The fastest path to approval is to seek pre-approval, gather your documents in advance, and apply through a broker with a wide lender panel. Tow Finance Solutions partners with more than 40 lenders and delivers approvals in as little as one hour.

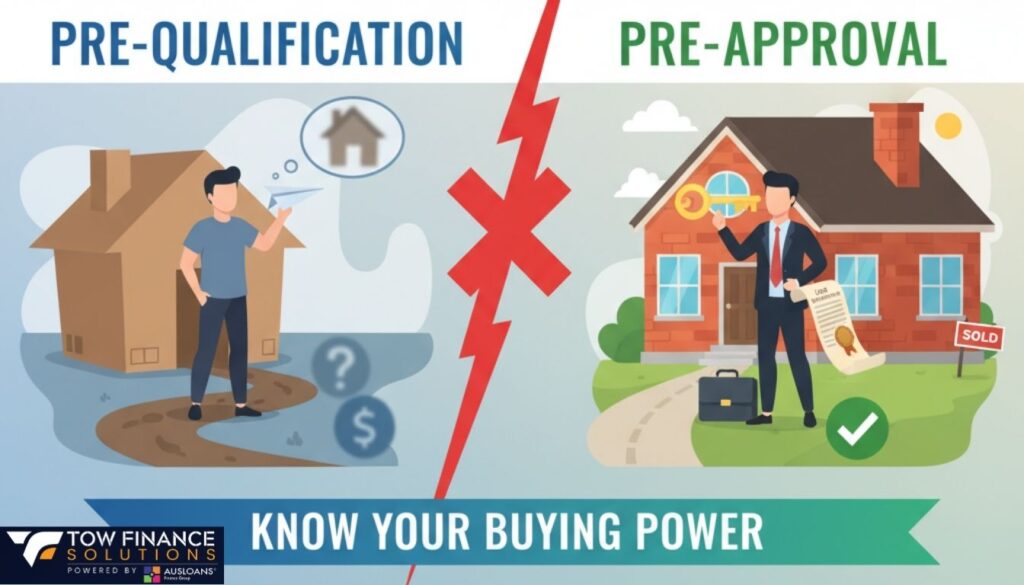

Pre-approval tells you exactly how much you can spend before you start negotiating with a dealer. Pre-approval typically lasts 30 to 90 days and does not lock you into a specific loan. Understanding the difference between pre-qualification and pre-approval helps you use each at the right stage. Finder

Documents you will generally need:

- Photo identification (driver licence or passport).

- Proof of income (recent payslips or, if self-employed, tax returns and bank statements).

- Details of the hybrid caravan (purchase price, make, model, year).

- A summary of existing debts and living expenses.

A secured loan can also cover registration, insurance and accessories such as solar, annexes and extra batteries, provided the total stays within the lender’s limit. Watch the fine print, because hidden fees can quietly raise your real cost.

Frequently Asked Questions

What interest rate will I pay on a hybrid caravan loan?

Secured caravan loan rates generally range from about 5.35% to 14.99% p.a., depending on the van’s age, your credit profile and the loan term. New-model loans averaged 8.65% p.a. in 2025, while used models averaged 11.93% p.a. Fixed rates keep repayments stable for the full term.

What loan term can I get on a camper trailer?

Hybrid caravan and camper trailer loan terms usually run from one to seven years. Shorter terms mean higher monthly repayments but less total interest, while longer terms ease cash flow at a higher overall cost. A loan calculator helps you compare both.

Do I need a deposit to finance a hybrid caravan?

No deposit is required in most cases. Secured caravan loans commonly fund up to 100% of the van’s value, and some lenders allow you to borrow above that to cover accessories. A deposit or trade-in still lowers your repayments and total interest.

Should I choose a secured or unsecured loan?

A secured loan is the better choice for most buyers because it carries a lower rate, using the van as collateral. An unsecured loan offers more flexibility for extras but charges higher interest. Read our secured vs unsecured guide to decide.

Can I finance a used hybrid caravan?

Yes. Used hybrids are cheaper to buy and finance, though rates run higher, averaging around 11.93% p.a. in 2025. Some lenders cap the van’s age, often requiring it to be under 10 years old at the end of the loan term, so check eligibility before you commit.

How fast can I get approved?

Approvals can be issued in as little as one hour through a broker with a wide lender panel. Having pre-approval and your documents ready speeds the process considerably. Our approval odds guide shows how to strengthen your application.

Can the loan cover accessories like solar and annexes?

Yes, within limits. A secured loan can usually fund registration, insurance, solar, annexes and extra batteries, as long as the total stays within the lender’s cap. If you want more than the secured limit allows, a separate unsecured loan can cover the difference.

Ready to Hit the Road?

Hybrid caravans deliver the rare combination of off-road freedom and home comforts, and the right finance structure makes ownership genuinely affordable. With access to more than 40 lenders and approvals in as little as one hour, Tow Finance Solutions matches you to a competitive, fixed-rate loan built around your budget.

Get your free hybrid caravan finance quote today or call (07) 4410 3375 to speak with a specialist.

Sources